Rich vs Poor Planning: The Power of Dynasty Trusts

Rich Planning and Poor Planning lead to very different families. I saw it firsthand. With Poor Planning, my family suffered a terrible probate when my grandfather passed away. It destroyed my family. My dad, uncle, and grandma litigated each other to death in probate court. My grandfather’s legacy was shattered. There was no peace. Our family was left in pieces.

After that, my mother married into a family who had great estate planning. I experienced Rich Planning. In my new family, our patriarch relocated from a high-tax, trust-unfriendly state to Florida. He established a dynasty trust, effectively preserving the family’s wealth for multiple generations.

This article compares New York vs Florida dynasty trusts to show how proper legal structures can safeguard your legacy for generations. I became a lawyer to promote Rich Planning and fix problems caused by Poor Planning. I help families experiencing the results of Poor Planning by litigating in probate court. I help affluent families implement Rich Planning to protect and grow their legacies.

My Experience With New York vs Florida Dynasty Trusts

I am a Florida estate planning and probate attorney with nearly a decade of experience (my firm opened in 2016). In my practice, I’ve witnessed how different state laws can make or break a family’s long-term legacy. Clients come to me after experiencing heartbreak in states like New York – where antiquated laws and high taxes chip away at what they built – and I’ve helped them reposition their plans to Florida’s more favorable legal landscape. I’ve also guided lifelong Floridians in leveraging our state’s unique benefits to create robust dynasty trusts that span generations. My goal is always the same: to use my expertise to secure your family’s future. I’ve seen both disaster and success, and I know which legal strategies truly work. Let’s dive into what I’ve learned.

New York’s Dynasty Trust Limits: The 21-Year Rule Explained

When comparing New York vs Florida dynasty trusts, New York’s perpetuities rule creates a clear disadvantage for long-term legacy planning. New York still follows the traditional Rule Against Perpetuities (RAP) in its strict form, a rule that limits how long a trust can last. This old rule, a “hangover from Elizabethan England,” is archaic in the extreme. In plain English, it means any trust in New York must be structured to vest (i.e. legally pass to beneficiaries) no later than 21 years after the death of someone alive at the time the trust was created. In practice, that typically works out to a maximum lifespan of roughly 90–100 years for a trust – often much less. For wealthy families looking to create a lasting legacy, this is a serious limitation.

How New York’s 21-Year Rule Ends Generational Trusts Early

Under New York’s Estates, Powers & Trusts Law, a trust is void from the start unless it must vest or end within “lives in being plus 21 years”. What does that mean? Essentially, you pick a person (or several people) who are alive when you create the trust – commonly your children or grandchildren – and the trust can’t continue more than 21 years after the last of those people passes away. This is New York’s Rule Against Perpetuities (sometimes called the “lives in being plus 21 years” rule).

For example, if you establish a trust in New York in 2025 and name your children as measuring lives, and the last surviving child dies in 2080, the trust must terminate by 2101 at the latest. That’s about 76 years from creation. Even if you tried to maximize the timeline by naming a newborn grandchild in 2025 as the measuring life, and that grandchild lives to, say, 100 years old, the trust would still end by around 2121 – roughly 100 years after creation. In other words, New York law forbids truly perpetual or “dynasty” trusts. It puts a legal expiration date on your family trust, whether you like it or not.

Why is this a big deal? Because when that clock runs out, the trust assets typically have to be paid out to the beneficiaries. Once distributed, those assets lose the protective wrapper of the trust. They become part of the beneficiaries’ own estates – and can be subject to estate taxes when the beneficiaries die, or become vulnerable to creditors, divorces, and lawsuits. New York’s perpetuities rule effectively forces wealth out of the trust and into the taxable estate of the next generation. As one commentator put it, historically you could put assets in a trust to avoid estate taxes temporarily, but “after a while the Rule Against Perpetuities would force the trusts to end. The assets would then be distributed…meaning that the assets would be subject to estate tax when the beneficiaries died.” In short, New York’s law can derail the very purpose of a dynasty trust – which is to skip estate taxes over multiple generations and keep assets protected long-term.

New York’s refusal to modernize this rule stands in stark contrast to many other states. In fact, “many states have thrown out the rule” entirely, but New York has not. The traditional RAP is famously convoluted (it’s the “bane of law students everywhere,” as one New York attorney quipped), and it’s arguably out of step with modern wealth planning needs. For wealthy New York families, it means you cannot easily create a trust that benefits your great-grandchildren or beyond – at least not without that trust ending and forcing a handoff of assets along the way.

The lesson from New York: If you keep your estate plan in a jurisdiction with a strict perpetuities law, your long-term wishes expire. The law in New York literally doesn’t allow you to lock in a legacy beyond a relatively short horizon. As we’ll see, this is one reason many families look for alternatives in more trust-friendly states.

New York Estate Tax: A Barrier to Dynasty Trust Success

Adding insult to injury, New York is also a tax-heavy state for wealthy estates and trusts. Unlike Florida, New York imposes a state estate tax on top of the federal estate tax. The New York estate tax rate can be up to 16% of the estate’s value – a significant bite. While New York does offer an estate tax exclusion amount (approximately $7.16 million per person in 2025), it comes with a nasty surprise: the infamous “cliff.” If your estate exceeds 105% of the exclusion (just roughly $7.5 million under current law), New York yanks away the entire exemption. In other words, if you go just a hair over the limit, your whole estate is taxed from dollar one – not just the portion above the exemption. This can result in a sudden and dramatic tax bill. For example, an $8 million New York estate might owe over $1.2 million in NY estate tax, whereas a $7 million estate would owe $0. It’s an all-or-nothing design, meaning moderately wealthy New Yorkers who slightly exceed the limit get no break at all.

Now consider how this interacts with New York’s trust limitations. Suppose you set up a trust for your children in New York and it grows substantially. When that trust inevitably ends (thanks to the RAP rule), those assets may pour into your children’s estates. If the amounts are above New York’s exemption, the state tax man is waiting at the door. And remember, the federal estate tax (40% top rate) might also apply if the assets are large enough – New York’s tax is in addition to federal. So, a family that thought their wealth was safely in trust could find as much as 50% or more of it gobbled up by taxes as it passes to the next generation (40% federal + 16% NY, roughly). This is precisely the scenario wealthy families fear – and rightly so.

It doesn’t end there. New York also has a state income tax that can affect trusts during their existence. If a trust is considered a New York resident trust (for example, if it’s created by a New York resident and has New York trustees or assets), any undistributed income the trust earns each year could be subject to New York fiduciary income tax. New York’s top income tax rate is around 10.9% (and even higher if you count New York City taxes) on high incomes. Trusts reach top tax brackets at very low income levels (just a few thousand dollars of income), so a trust paying New York income tax could easily lose ~10% of its investment earnings to the state annually. That’s money that won’t be compounding for the future beneficiaries. In Florida, by contrast, trusts owe no state income tax on their earnings – a huge long-term savings. We’ll talk more about Florida in a moment, but it’s important to recognize that staying in a high-tax state like New York creates a drag on growth every year and then wallops you again at each generational transfer.

In summary, New York’s legal environment for trust planning is hostile to the idea of a dynasty trust. The rule against perpetuities forces your trust to expire within a few generations, and New York’s estate tax and income tax siphon off wealth along the way. A New York estate plan can truly become a “legacy limiter.” Fortunately, there’s a better path for those willing to look south – specifically, to Florida.

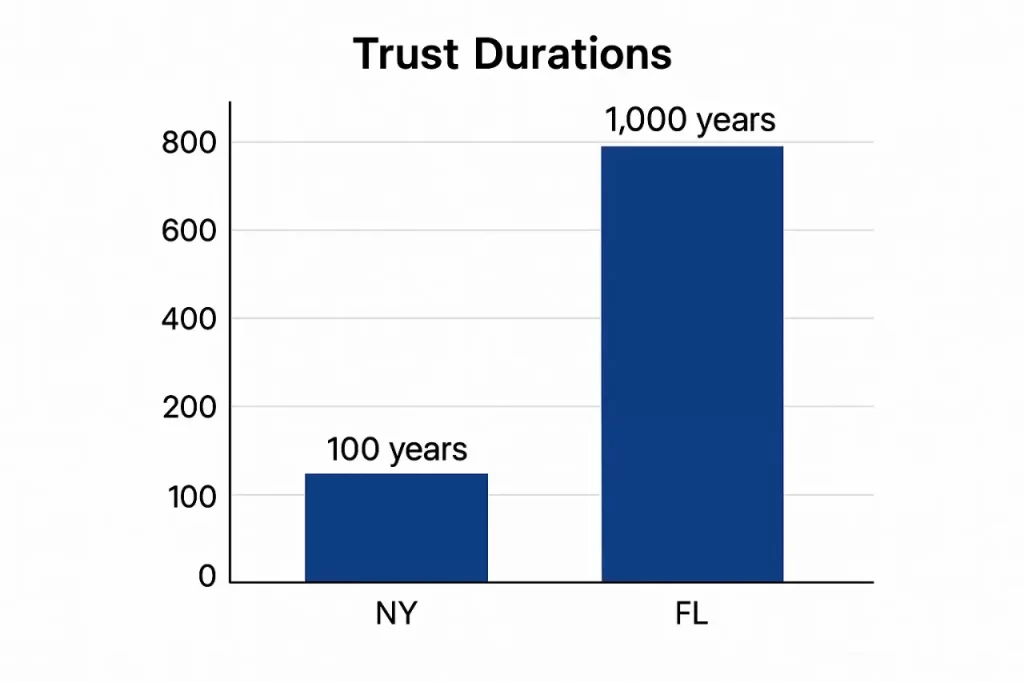

Graph: Maximum Trust Duration Allowed by Law in New York vs Florida. New York’s traditional rule (lives-in-being plus 21 years) effectively caps a trust’s life at roughly 90–100 years, often ending by the grandchildren’s generation. Florida, however, has modernized its law to allow trusts to last up to 1,000 years – essentially letting you create a near-perpetual dynasty trust. This stark difference means a Florida trust can serve many more generations of your family than a New York trust ever could.

Why Florida Is the Best State for Dynasty Trusts

Florida is often hailed as a trust-friendly paradise, and for good reason. Over the past two decades, Florida has actively reformed its laws to accommodate long-term trusts and to attract wealthy individuals looking for a better environment for their assets. I moved my own practice and advise my clients to take advantage of Florida’s unique combination of legal and tax benefits. Let’s break down why Florida is such a great choice for a dynasty trust.

Florida’s 1,000-Year Trust Law: Multigenerational Wealth Protection

Florida has essentially done what New York refuses to do: throw out that old 21-year rule. In 2022, Florida amended its Statutory Rule Against Perpetuities (Florida Statutes § 689.225) to extend the permissible duration of trusts to a staggering 1,000 years. For any trust created on or after July 1, 2022, an interest can vest as far as 1,000 years from when the trust is created. (Florida had already extended its limit from the common 90 years to 360 years back in 2000; the new law expanded it further to 1,000 years for modern trusts.) In practical terms, this means Florida trusts can endure for millennium – effectively forever for a human family’s purposes.

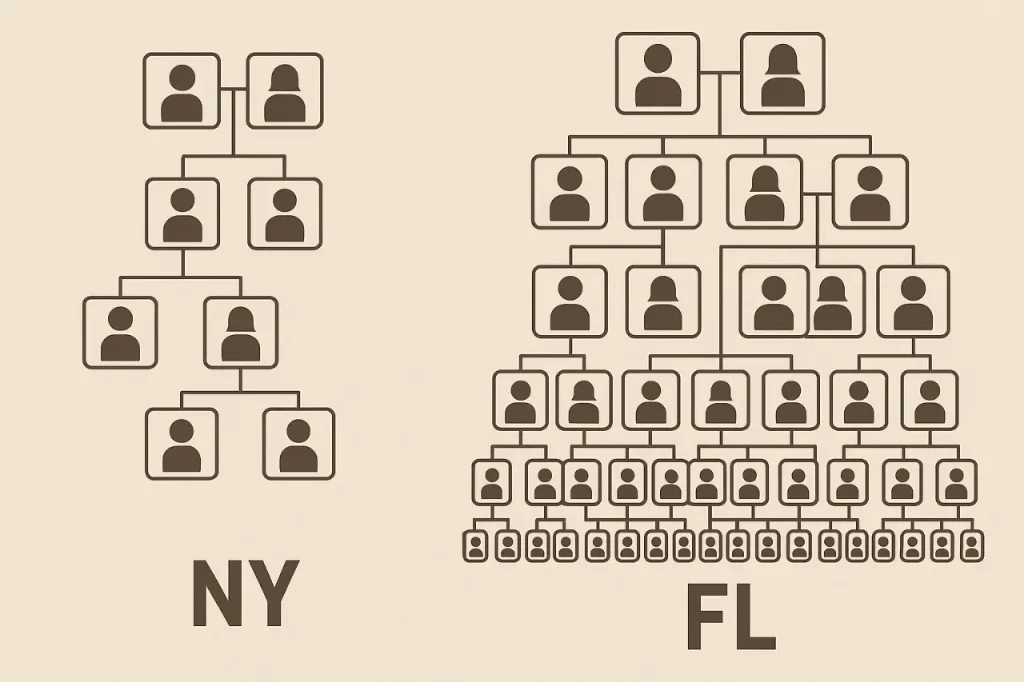

Let that sink in: if you establish a dynasty trust under Florida law, you can realistically plan for many generations of descendants – not just your children and grandchildren, but their great-grandchildren and so on, potentially into the 30th generation and beyond. The law won’t force your trust to terminate in the lifetime of anyone alive today. One of the clearest advantages in the New York vs Florida dynasty trusts debate is Florida’s 1,000-year lifespan for trusts compared to New York’s 90–100-year cap. (For instance, Nevada allows 365-year trusts and South Dakota 500-year trusts – Florida has outdone them with 1,000 years.)

From an estate planning perspective, this is a game-changer. With a Florida dynasty trust, you can keep assets in trust across multiple generations without ever triggering estate taxes at each generational pass. How? Because if the trust never fully distributes assets and ends, those assets aren’t included in each beneficiary’s taxable estate upon their death. The tax savings over time are enormous. As one estate planning analysis noted, abolishing the Rule Against Perpetuities solves this problem – you can “gift assets to a trust, get them out of your estate, and then avoid transfer taxes forever”. Florida’s law comes very close to abolishing the rule entirely (1,000 years is essentially perpetual for our purposes). That means a properly set-up Florida dynasty trust, combined with wise use of your federal Generation-Skipping Transfer (GST) tax exemption, could shield your family’s wealth from estate and gift taxes for centuries. Instead of the IRS and state tax authorities taking a cut every generation, your trust assets continue growing and benefiting your heirs.

Furthermore, keeping assets in trust for generations provides creditor protection and control benefits. Because the trust, not the individual heirs, owns the assets, those assets are generally protected from beneficiaries’ creditors or divorcing spouses. And the trust can be structured with detailed instructions or incentives that reflect your family’s values, encouraging responsible use of wealth. Florida’s long-duration trust capability means those protective features and family governance can last far into the future, truly creating a lasting legacy.

In short, Florida’s modernization of the perpetuities rule enables Rich Planning at its finest: the ability to create a family bank that survives for ages. Instead of your legacy being sliced into pieces by mandatory distributions and taxes, it can remain whole and growing under the stewardship of trustees you choose, for generation after generation.

Florida’s Tax Perks for Dynasty Trust Planning

Legal changes alone wouldn’t be as attractive without Florida’s extremely favorable tax climate. This is where Florida leaves New York in the dust. Florida imposes no state income tax, no estate tax, and no inheritance tax on individuals or on trusts. It’s one of the most tax-friendly states in the nation, which is a key reason so many wealthy families and family offices relocate here.

Let’s unpack that:

- No State Income Tax: Florida is one of only a handful of states with no personal income tax at all. This means if you, as an individual, become a Florida resident, your income (including retirement income, investment income, etc.) isn’t taxed by the state. But equally important, a trust administered in Florida (with no New York ties) also pays no Florida income tax on its earnings. Compare that to New York, where trust income often faces the ~10% state tax. Over years, not having to pay state tax on trust investment gains can keep significantly more wealth compounding for your beneficiaries.

- No Estate or Inheritance Tax: Florida has no state estate tax – it was effectively repealed in 2005 when the federal credit for state death taxes ended. If you die as a Florida resident, your estate owes nothing to the State of Florida, no matter how large your estate is. (Only the federal estate tax, if applicable above the multi-million-dollar federal exemption, would apply.) Likewise, Florida has no inheritance tax on beneficiaries. New York, as we discussed, can take up to 16% of an estate and has that brutal cliff rule. Florida takes 0%. This is a monumental difference. To put it plainly: a wealthy family can save millions in taxes simply by shifting their domicile and estate plan to Florida. One prominent law firm describes Florida’s freedom from “death taxes” and income tax, combined with its warm climate, as making it “an attractive destination to relocate, especially for wealthy individuals wanting to reduce their tax liability.” I couldn’t have said it better myself – Florida welcomes you and your wealth, whereas some other states seem to punish you for dying or prospering.

- Homestead and Other Perks: Beyond trusts, Florida also offers generous homestead protections for your primary residence (creditor protection and property tax caps), no state capital gains or dividend taxes, and overall a pro-business, pro-investor environment. While this article is focused on dynasty trusts, it’s worth noting that moving to Florida can carry a whole package of financial benefits for someone of means. These ancillary benefits often sweeten the deal for my clients considering a relocation. It’s not just about what Florida doesn’t take from you; it’s also about the protections and peace of mind Florida gives you.

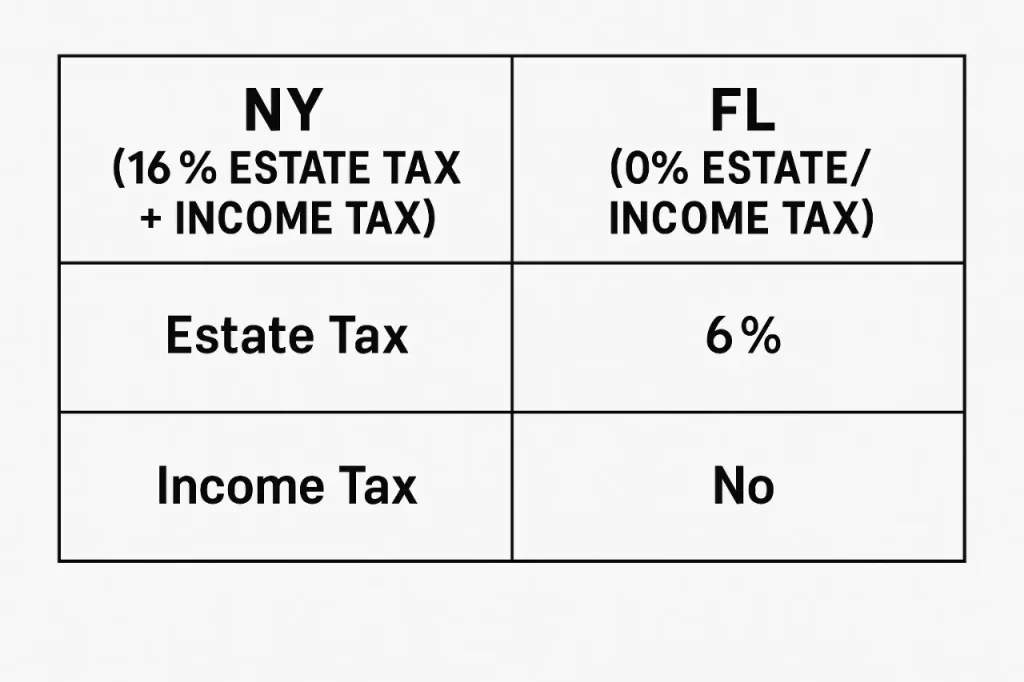

Graph: State Tax Comparison – New York vs Florida. The chart above highlights the stark tax differences. New York imposes up to a 16% estate tax on large estates and a top state income tax near 10.9% on individuals (and by extension, high trust income), whereas Florida imposes 0% – no estate tax and no income tax. This means a New York-based family’s wealth faces extra state taxation both when it grows (income tax each year) and when it passes to heirs (estate tax at death), while a Florida-based family avoids those state taxes entirely. Over multiple generations, Florida’s tax advantage can preserve substantially more of your wealth within the family.

Considering both the legal and tax angles, it’s clear why Florida is a top choice for establishing a dynasty trust. You get the ultra-long duration allowed (so the trust can function as a multigenerational financial fortress), and you eliminate the state-level taxes that erode your fortune. It’s the combination of time and tax benefits that really supercharge “Rich Planning” in Florida.

Of course, simply moving to Florida or setting up a trust here isn’t a magic wand – it must be done correctly. If you’re relocating from a state like New York, you need to properly establish Florida domicile (e.g., change your primary residence, update voter registration, driver’s license, etc.) and likely update your estate planning documents to Florida law. Trusts may need to be moved or decanted to Florida with care to avoid triggering taxes during the move. The good news is, with experienced legal guidance, these steps are very achievable. I have helped many clients abandon their former high-tax domicile and smoothly transition their planning to Florida. The result is often an immediate sense of relief – they know their legacy is now anchored in a state that will help, not hinder, their goals.

Let’s illustrate these lessons with a concrete example.

Example: Two Families, Two States, Two Very Different Outcomes

A Patriarch, age 75, is the head of a successful family business and has a substantial estate. He has a Daughter and a Son, both in their 40s, and several young grandchildren. The Patriarch created a trust in New York years ago as part of his estate plan, intending for the trust to provide for his children and future descendants. The trust’s terms say it will continue for his grandchildren’s benefit until they are adults and then terminate, distributing assets to them outright.

As the Patriarch grows older, he becomes concerned about two things: (1) the New York trust will eventually terminate, potentially during his grandchildren’s lifetime, and (2) a significant portion of his wealth could be lost to taxes. He remembers that his own father’s estate, years ago, had been hit by New York’s estate tax, and it still bothers him how much the family paid to the state.

The Patriarch consults with his estate attorney (that’s me). I explain that under New York’s rule against perpetuities, his trust indeed cannot last beyond 21 years after the death of his children (who are the measuring lives in his trust). That means, at best, the trust might run until a bit after his children’s generation, then must end. When it ends, all remaining assets will be handed over to the beneficiaries (his grandchildren, or great-grandchildren if any by then). Those assets would then be in their personal estates.

We walk through a scenario: Suppose the trust ends when the Patriarch’s youngest grandchild turns 25, which might be 30 years from now. At termination, the trust has, say, $50 million of assets remaining. Under New York law at that time, each beneficiary’s share could be subject to New York estate tax when that beneficiary eventually dies. If one grandchild receives $25 million and later dies a New York resident, New York could easily take 16% of that (around $4 million) in state estate tax, in addition to federal estate tax. Moreover, once that money is out of the trust, it’s exposed – a creditor or lawsuit against a grandchild could reach it, or it might be squandered or mismanaged.

The Patriarch is alarmed. He wants this scenario to be avoided. I then present an alternative: move the wealth into a Florida dynasty trust before those events happen. We discuss creating a new trust under Florida law that could last for generations – effectively a trust that his great-great-grandchildren could one day benefit from. We also discuss him relocating his residency to Florida to take advantage of the tax benefits personally.

Motivated by protecting his legacy, the Patriarch takes action. He purchases a home in Florida, establishes it as his domicile, and moves his legal residence. He transfers a large portion of his assets, including interests in the family business and investments, into a newly established Florida dynasty trust. The trust is designed to benefit Daughter, Son, grandchildren, and future descendants, but crucially, it does not have to terminate after a certain date – it can continue for up to 1,000 years. The trust includes provisions to skip any beneficiary who might be fiscally irresponsible, ensuring the wealth is managed prudently over time. A trusted Banker (a family-friendly trust company in Florida) is appointed as a co-trustee alongside Daughter, providing professional management.

Shortly after these changes, the difference is palpable. The Patriarch’s Son, who still lives in New York, notices that the trust now pays no New York income taxes on its investment earnings (since it’s administered in Florida with no New York trustees or assets). The Son remarks that the trust’s earnings seem to be growing faster without that annual tax drag. The Daughter, who moved to Florida with her father, feels relief that her future inheritance in the trust won’t face a state death tax.

Years later, the Patriarch passes away as a Florida resident. Because of Florida’s laws, no state estate tax is due – only a federal estate tax return is filed. His New York real estate had been sold or placed in entities, so New York has little claim on his estate. The dynasty trust he created continues seamlessly after his death, managed by the co-trustees for the beneficiaries.

As time goes on, the trust distributes income to the Daughter and Son for their needs, but the principal largely stays intact, investing and growing. When the Son (who remained in New York) eventually dies, the assets in the Florida trust that benefit his children are not part of the Son’s taxable estate – they belong to the ongoing trust. Thus, New York cannot tax those assets, and they pass free of estate tax to the next generation. The Judge who oversees the Son’s New York probate notes that the Son’s own estate was relatively modest since most wealth was in the trust, which avoided a multi-million-dollar New York tax that would have applied had the Patriarch done nothing.

Meanwhile, the Daughter lives comfortably in Florida on trust distributions. She appreciates that even if she were to be sued or if she had a rocky marriage, the trust assets are generally shielded – a legacy of her father’s foresight. The trust will continue after Daughter’s lifetime for her children (the Patriarch’s grandchildren and great-grandchildren), with a Family Office advisor and the corporate trustee managing it. Decades later, the family’s business and investments are still held in that trust, supporting various family members’ ventures – from paying for great-grandkids’ education to funding new businesses – all according to the Patriarch’s guiding wishes. The wealth has not been diluted by estate taxes at each generation, thanks to the long-term Florida trust structure.

In contrast, the Patriarch’s Brother, who stayed in New York with a similarly sized estate, passed away around the same time. His estate had a standard New York trust that ended at his children. By the time the Brother’s assets reached his grandchildren, New York estate taxes and forced distributions had substantially reduced the pot. The Brother’s family had to sell a beloved vacation property to cover the tax bill, and the remaining inheritance was split outright among heirs who handled it with varying degrees of success. One grandchild’s share was lost in a lawsuit; another grandchild quickly spent his portion on unwise investments. Within a generation, most of the Brother’s legacy was either taxed or dissipated.

This Example paints a clear picture: the Patriarch who embraced Florida’s dynasty trust approach saw his family’s wealth protected and growing, whereas the one who remained under New York’s restrictive rule saw much of his legacy lost. The difference came down to legal strategy – choosing the right jurisdiction and tools for the job.

Breakdown: How Florida Dynasty Trusts Beat New York Trust Limits

Let’s break down the key lessons from the example and apply the law step by step:

1. New York Trust Termination vs. Florida Trust Continuance: In the example, the Patriarch’s original New York trust was destined to terminate once the measuring lives plus 21 years condition was met. This is dictated by New York’s rule against perpetuities (EPTL § 9-1.1) – no interests can vest beyond 21 years after a life in being. Practically, that meant the trust would end in the grandchildren’s generation. Once it ended, by law, the assets had to be distributed to beneficiaries outright. In the Florida trust, however, there was no such required termination in the grandchildren’s lifetime. Florida’s law (Fla. Stat. § 689.225 as amended) allowed the Patriarch to set up a trust that could last far beyond the lives of his children and grandchildren – up to 1,000 years. The effect is profound: the Florida trust does not face a legal “sunset” like the New York trust did. The Breakdown: if you want a trust to serve multiple future generations, New York law will cut that short; Florida law will not.

2. Tax Implications – Estate Tax “Cliff”: The Patriarch’s concern about New York estate tax was well-founded. In New York, if his estate (or eventually his son’s estate) exceeded the exclusion by even 5%, the entire estate value would be taxable at up to 16%. In our example, the Patriarch’s brother’s family felt this – they paid a hefty NY estate tax, forcing asset sales. Florida, conversely, has no estate tax. In the Patriarch’s Florida plan, when he died, the absence of a state estate tax saved potentially millions of dollars that stayed in the trust for his heirs. The breakdown: relocating to Florida and situs-ing the trust in Florida eliminated the state death tax that would have applied in New York, directly increasing the net legacy passed on.

3. Generation-Skipping (GST) Tax Planning: Although not explicitly mentioned in the story, it’s worth noting from a technical perspective. When the Patriarch moved assets into a dynasty trust, we would allocate his federal GST tax exemption to that trust. This means those assets can skip down multiple generations free of federal GST tax (which is 40%, analogous to the estate tax, on transfers to grandchildren or beyond). The trust is designed to skip inclusion in each generation’s estate. New York’s RAP would ordinarily stop such a strategy because the trust can’t last long enough to skip multiple generations – but Florida’s law enables it. By combining Florida’s long trust duration with GST exemption allocation, the trust assets avoid both state estate tax and federal estate/GST taxes as they pass down the line. In breakdown: Florida law provides the time horizon needed to fully exploit generation-skipping tax strategies, whereas New York law would force a taxable event relatively early.

4. Income Tax Savings Over Time: The example noted the New York son observing no New York income tax on the Florida trust’s earnings. To clarify, when the trust moved to Florida, it likely became a non-resident trust for New York tax purposes (no NY trustees or assets, and the grantor was no longer NY domiciled). Thus, New York stopped taxing its income. Florida doesn’t tax it either. The result: the trust’s interest, dividends, and capital gains are taxed only at the federal level, not state. If the trust earns $1 million in a year, that’s about $100k of state tax saved annually (compared to if it were taxed in NY). Over decades, compounding that extra $100k per year makes a huge difference. Breakdown: Florida not only saves one-time estate taxes, but also provides ongoing annual tax savings, boosting growth.

5. Asset Protection and Control: When the Patriarch’s trust remained intact in Florida, it continued to shield assets from beneficiaries’ potential issues. In New York, once the trust ended, each beneficiary’s share was theirs outright – and could be lost to lawsuits or bad decisions (as happened with the Brother’s grandchildren). Florida law generally respects spendthrift trust provisions and allows long-term trusts to maintain those protections. Additionally, Florida has robust trust codes for decanting and directing trusts, meaning if changes or adaptations are needed, Florida law gives tools to adjust the trust without court fights. Breakdown: a Florida dynasty trust can adapt and protect, whereas a terminated New York trust leaves assets unprotected in beneficiaries’ hands. The prolonged structure under Florida law is inherently more protective.

6. Relocation and Domicile Matters: The example underscored that the Patriarch himself changed his domicile to Florida. This was crucial. Had he remained a New York resident, New York would attempt to tax his worldwide assets at death (including those in a trust he created, depending on trust structure). By becoming a Floridian, he cut that tie. However, just owning a Florida trust isn’t enough – changing domicile is key to fully escape the old state’s taxes. We always advise clients on the formalities of abandoning the old domicile and establishing Florida residency: filing a Florida Declaration of Domicile, registering to vote in Florida, getting a Florida driver’s license, etc. In breakdown: the legal benefits of Florida can be fully realized only if you genuinely make Florida your home base. Paperwork and proper planning ensure that New York (or any other state) cannot pull the estate back into its tax regime.

The following legal and tax takeaways further highlight the impact of choosing wisely between New York vs Florida dynasty trusts. Poor Planning was sticking with the status quo in a high-tax, trust-restricted state – resulting in loss of control and wealth to the government and outsiders. Rich Planning was proactively moving to a favorable jurisdiction (Florida) and using its laws to the family’s advantage – resulting in preservation of wealth, control, and long-term security.

Every family’s situation is unique, of course. New York’s rule might not ruin a smaller estate, and Florida’s trusts aren’t one-size-fits-all. But for affluent families aiming to build a dynasty – a legacy that endures – the verdict is clear: Florida is far superior to New York. The laws here align with your goals, not work against them.

Why Dynasty Trusts Are Personal to Me

I share these insights not just as an attorney, but as someone who has lived the difference between poor planning and rich planning. I know what it’s like to watch a loved one’s legacy fall apart – my own family went through that pain, and it left scars. That experience is what drives me every day to fight for my clients’ families, to find solutions that prevent heartbreak and conflict. When I moved to Florida and saw the powerful tools this state offers for legacy building, I felt hope that no family should have to repeat my family’s story.

In my years of practice, I’ve stood in probate court consoling a Son or Daughter who lost half their inheritance to infighting and taxes – and I’ve also sat at a patriarch’s kitchen table in Miami, mapping out a dynasty trust that brings a smile and tears of relief to his face because he knows his grandchildren will be taken care of long after he’s gone. I love those moments – when a client realizes “We’re going to be okay. Our legacy is safe.” It’s why I do what I do.

Trust law and taxes can sound dry on paper, but to me, they’re the architecture of real people’s lives and dreams. Every trust I draft, every plan I craft, carries the weight of a family’s hopes. I take that responsibility to heart. I also understand the human side – the emotions, the family dynamics, the values at stake. My approach is not just to be your lawyer, but to be your partner in legacy-building. I speak in plain language, I make sure you understand each step, and I always remember that behind every “trust” or “estate” is a family and a story.

If you’re reading this as a 65+ family leader or someone managing a family office, I want you to know: I respect what you’ve built. You’ve worked hard, you’ve overcome challenges, and you care deeply about what happens to it all when you’re gone. I’m here to ensure your story has a secure and thriving next chapter. Let’s take the rich-planning route together. You don’t have to navigate these complex decisions alone. I’ll bring the expertise and the heartfelt commitment to protect your family’s future – you bring the vision of what you want that future to be. Together, we’ll make it happen.

You have three ways to get in touch with me:

- Call me at (305) 634-7790 – I’m available to discuss your concerns and goals.

- Email me at JO@JOValentino.com – Send me your questions or a brief overview of your situation, and I’ll personally respond.

- Fill out the contact form on my website at JOValentino.com/contact – I’ll review your submission and reach out to schedule a consultation.

I genuinely look forward to hearing from you and exploring how we can protect your family’s legacy.

Disclaimer

This article is for informational purposes only and does not constitute legal advice or create an attorney-client relationship. Reading this does not make me your lawyer – I can only accept that role through a signed written agreement with you, after we’ve both agreed to it. Every situation is unique, and laws change. Please consult me (or another qualified attorney) for advice tailored to your specific circumstances. Until you receive a signed writing from me confirming I’ve agreed to be your attorney, please do not assume any guidance here applies to your exact situation. I am licensed in Florida, and any references to laws are based on the current statutes and rules as of the time of writing. I strive for accuracy, but I cannot guarantee that all information here remains up-to-date or applicable to all readers. In short: Let’s talk one-on-one before making big decisions. I’m here when you’re ready.

Thank you for reading, and I wish you and your family the very best in wealth, health, and happiness.

Recommended Books on Dynasty Trusts and Estate Planning

For more in-depth strategies and guidance, you can download my free e-books (PDF):

- The Essential Guide to Florida Estate Planning: Protecting Your Legacy and Family

- Star-Spangled Planner: Protect Your Family and the Second Amendment with Estate Planning

- Global Family’s Guide to US Inheritance Law – The Gold Card Advantage

- The Florida Realtor’s Guide to Probate Properties: From Listing to Closing

Each of these books is packed with insights and practical tips stemming from my experience. Feel free to read and share them.

Learn Estate Planning Through Celebrity Dynasty Trust Mistakes

I believe learning about estate planning doesn’t have to be dull. I often comment on celebrity estate news to make these lessons engaging. Check out my short videos on social media – it’s a fun way to see real-world examples of planning pitfalls and successes:

- Facebook: Follow my page for regular video updates – JOValentino on Facebook

- YouTube Shorts: Subscribe to my channel – @JOValentino on YouTube for quick, informative shorts.

- Instagram: Follow @ValentinoJOV on Instagram for bite-sized estate planning wisdom and news commentary.

- Twitter (X): Follow me on X (Twitter) @JesusOValentino for timely insights and links to interesting cases and articles.

Stay informed and entertained – and remember, rich planning is the key to peace of mind for you and prosperity for those you love.

FAQs

What is the key difference between New York and Florida dynasty trusts?

Florida allows trusts to last up to 1,000 years. New York requires trusts to end within 21 years after the death of a measuring life, limiting long-term protection.

Why does the Rule Against Perpetuities matter in estate planning?

It limits how long a trust can shield assets. New York’s rule forces trust termination in 1–2 generations, exposing assets to taxes and creditors.

Can I move my New York trust to Florida?

Possibly, through a process called “decanting” or trust migration. Work with an attorney to ensure it’s done legally and tax-efficiently.

What tax savings does a Florida dynasty trust offer?

Florida imposes no state income or estate tax. Trust income grows faster, and multigenerational transfer taxes are minimized or eliminated.

Do I need to change my domicile to benefit from Florida trust law?

While not always required, changing domicile strengthens your legal position and can avoid estate tax liability in your original state.

Share: